|

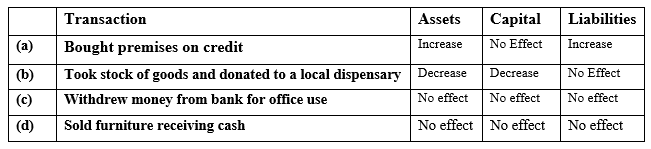

Mention whether the following transactions have an increase, decrease or no effect on the assets, capital and liabilities of a business. (4 mks)

1 Comment

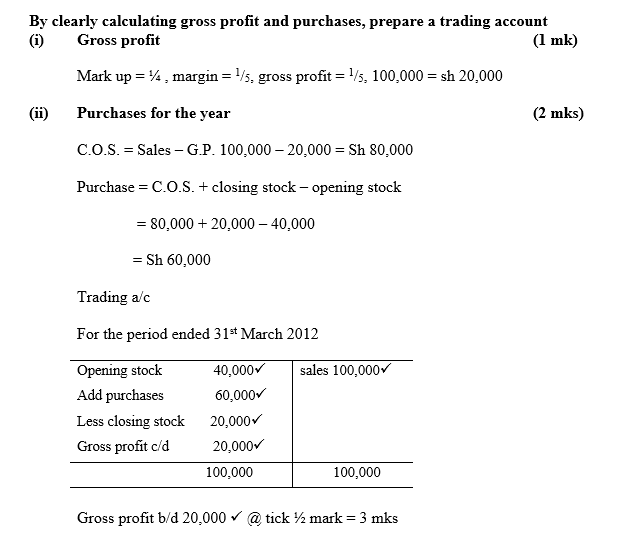

The following information relates to Liston traders for the period ended 31st March 2012.The following information relates to Liston traders for the period ended 31st March 2012.

The following information was extracted from the books of Dawida business enterprise for the year ended 30th June 2000.

FINANCIAL STATEMENTS - KCSE BUSINESS STUDIES NOTES, AUDIOVISUALS, QUESTION AND ANSWERCONTENTS

SPECIFIC OBJECTIVESBy the end of the topic, the learner should be able to:

Financial StatementsThese are prepared at the end of a given trading period to determine the profit and losses of the business, and also to show the financial position of the business at a given time. They includes; trading account, profit and loss account, trading profit and loss account and the balance sheet. They are also referred to as the final statements.

The trading period is the duration through which the trading activities are carried out in the business before it decides to determines it performances in terms of profit or loss. It may be one week, month, six months or even a year depending on what the owner wants. Most of the business use one year as their trading period. It is also referred to as the accounting period. At the end of the accounting period, the following takes place;

Determining the profit or loss of a businessWhen a business sells its stock above the buying price/cost of acquiring the stock, it makes a profit, while if it sells below it makes a loss. The profit realized when the business sell it stock beyond the cost is what is referred to as the gross profit, while if it is a loss then it is referred to as a gross loss.

It is referred to as the gross profit /loss because it has not been used to cater for the expenses that may have been incurred in selling that stock, such as the salary of the salesman, rent for the premises, water bills, etc. it therefore implies that the businessman cannot take the whole gross profit for its personal use but must first deduct the total cost of all other expenses that may have been incurred. The profit realized after the cost of all the expenses incurred has been deducted is what becomes the real profit for the owner of the business, and is referred to as Net profit. The net profit can be determined through calculation or preparation of profit and loss account. In calculating the gross profit, the following adjustments are put in place

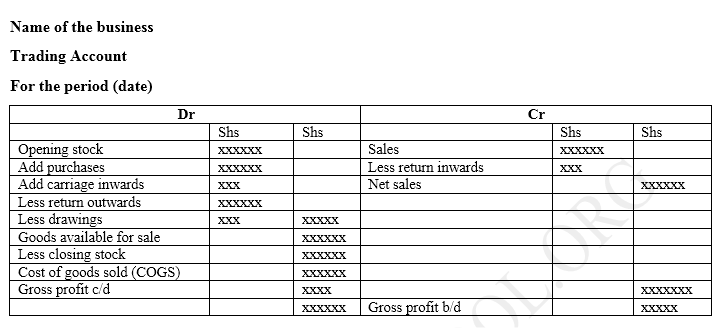

Trading AccountThis is prepared by the business to determine the gross profit/loss during that trading period

It takes the following format

The trading account is completed by the time the gross profit b/d is determined

For example The following balances were obtained from the books of Ramera Traders for the year ending may 31st 2010

Download below to continue reading ... (Learn how to download ...) financial statements questions & answers

|

Business Studies Notes Form 1 - 4

Categories

All

Archives

April 2024

AuthorAtika School Team |

||||

RSS Feed

RSS Feed